(以下任何觀點均為作者個人觀點,不應構成投資決策的依據,也不應被視為從事投資交易的推薦或建議。)

砰!砰!砰!

這是手機提醒我監測夜間北海道各滑雪場降雪狀況的聲音。雖然這種聲音在一月和二月給我帶來了巨大的快樂,但在三月它只帶來了 FOMO。

我三月初從北海道出發,度過過去的幾個滑雪季。我最近的經驗告訴我,大自然在 3 月 1 日左右開始升溫。我是滑雪初學者,只喜歡最乾燥、最深的斜坡。然而,這個賽季,蓋亞卻發生了巨大的變化。二月的一陣猛烈的暖浪驅走了積雪。寒冷的天氣直到月底才會回來。但三月的寒冷氣溫又回來了,每晚都會傾倒 10 至 30 公分的新鮮戰俘。這就是我手機爆炸的原因。

整個三月,我坐在東南亞各個炎熱潮濕的國家,愚蠢地查看應用程序,毀掉了我離開滑雪場的決定。四月的解凍終於真正發生了,我的 FOMO 也隨之結束了。

正如讀者所知,我的滑雪經驗是我的一般經濟學和加密貨幣交易書籍的隱喻。我之前寫過,3月12日美國銀行定期融資計畫(BTFP)終止將導致全球市場暴跌。 BTFP被取消,但加密貨幣產業的惡性拋售並未發生。比特幣果斷突破 7 萬美元,最高達到 7.4 萬美元左右。 Solana 繼續與各種小狗和小貓迷因代幣一起泵送。我的時機不好,但就像滑雪季節一樣,三月出乎意料的有利條件不會在四月重演。

雖然我喜歡冬天,但夏天也帶來歡樂。北半球夏季的到來帶來了運動的樂趣,我重新安排了時間去打網球、衝浪和風箏衝浪。由於聯準會和財政部的政策,夏季將出現新的法定流動性湧入。

我將簡要概述我的心智圖,說明風險資產市場將如何以及為何在四月經歷極度疲軟。對於那些敢於做空加密貨幣的人來說,整體經濟狀況是有利的。雖然我不會直接做空市場,但我已經平掉了幾個垃圾幣和 memecoin 交易頭寸並獲利了。從現在到 5 月 1 日我將處於非貿易區。我希望能在五月回來,帶著準備部署的乾火藥,為牛市真正開始做好準備。

詐欺罪

The Bank Term Funding Program (BTFP) ended a few weeks ago, but U.S. too-big-to-fail (TBTF) banks have not faced any real pressure subsequently. This is because the high priests of Fugazi Finance have a range of tricks they will use to secretly print money to bail out the financial system. I will take a peek behind the scenes and explain how they are expanding the USD fiat supply, which will support a general rally in cryptocurrencies and stocks until the end of the year. While the end result is always money printing, the process is not without periods of slower liquidity growth, which provides negative catalysts for risk markets. By carefully studying this series of techniques and estimating when the rabbit will be pulled out of the hat, we can estimate when the period will come when the free market is allowed to operate.

Discount Window

The Fed and most other central banks operate a tool called the discount window. Banks and other covered financial institutions in need of funds can pledge eligible securities to the Fed in exchange for cash. Overall, the discount window currently only accepts U.S. Treasuries (UST) and mortgage-backed securities (MBS).

Let's say a bank got screwed because a bunch of Pierce and Pierce boomer puppets ran it. The bank's holdings of UST were worth $100 when purchased, but are currently worth $80. Banks need cash to meet deposit outflows. Insolvent shit banks could use the discount window instead of declaring bankruptcy. The bank exchanges $80 of UST for $80 of U.S. dollar bills because, under current rules, the bank receives the market value of the pledged security.

In an effort to repeal the BTFP and remove the associated negative stigma without increasing the risk of bank failure, the Federal Reserve and the U.S. Treasury are now encouraging troubled banks to take advantage of the discount window. However, under current collateral terms, the discount window is not as attractive as the recently expired BTFP. Let's go back to the example above to understand why.

Remember, the value of UST fell from $100 to $80, which means the bank had an unrealized loss of $20. Initially, $100 of UST is provided by a $100 deposit. But now UST is worth $80; therefore, if all depositors flee, the bank will be short $20. Under BTFP rules, banks receive the face amount of underwater UST. This means that $80 worth of UST would be exchanged for $100 in cash when delivered to the Fed. This restored the bank's solvency. But the discount window only offers $80 for $80 worth of UST. The $20 loss remains and the bank remains insolvent.

Given that the Fed can unilaterally change collateral rules to balance the treatment of assets under the BTFP and the discount window, by giving the insolvent banking system the green light to use the discount window, the Fed continues to engage in stealth bank bailouts. So the Fed essentially solves the BTFP problem; the entire UST and MBS balance sheet of the insolvent US banking system (which I estimate at $4 trillion) will be used to back loans if needed with funds printed from the discount window. This is why I believe the market did not force any non-TBTF banks into bankruptcy after the end of BTFP on March 12th.

bank capital requirements

Banks are often asked to provide funds to governments that issue bonds at yields below nominal GDP. But why would a private for-profit entity buy something with a negative real yield? They do this because banking regulators allow banks to buy government bonds with little or no down payment. When banks with insufficient capital buffers on their government bond portfolios inevitably collapse as inflation sets in and bond prices fall as yields rise, the Fed will allow them to use the discount window in the manner described above. . As a result, banks would rather buy and hold government bonds than provide loans to businesses and individuals in need of funds.

When you or I buy anything with borrowed money, we must pledge collateral or equity to cover potential losses. This is prudent risk management. But if you're a vampire squid zombie bank, the rules are different. After the 2008 global financial crisis (GFC), World Bank regulators sought to force global banks to hold more capital in order to create a more robust and resilient global banking system. The body of rules that codifies these changes is called Basel III.

The problem with Basel III is that government bonds are not considered risk-free. Banks must commit small amounts of capital to their large sovereign bond portfolios. These capital requirements prove problematic in times of stress. During the COVID-19 market crash in March 2020, the Federal Reserve decreed that banks could hold UST without the backing of collateral. This allows banks to step in and store trillions of dollars worth of UST in a risk-free way...at least as far as accounting is concerned.

When the crisis abated, UST's supplementary leverage ratio (SLR) exemption was reinstated. Predictably, as UST prices fell due to inflation, banks went bankrupt due to insufficient capital buffers. The Fed came to the rescue through BTFP and now the discount window, but that only made up for the losses from the last crisis. How can banks step up their game and absorb more bonds at current unattractively high prices?

The U.S. banking system loudly declared in November 2023 that as Basel III forced them to hold more capital in government bond portfolios, Bud. Gur. Yellen can't squeeze more bonds into them. So something has to give because the U.S. government has no other natural buyer of its debt with negative real yields. Here's how banks politely express their precarious situation.

Demand for U.S. Treasuries may have softened from some traditional buyers. Bank securities portfolio assets have been declining since last year, with banks holding $154 billion less in U.S. Treasury securities than a year ago.

Source: Treasury Borrowing Advisory Committee Report to the Secretary of the Treasury

The Fed, led by Jerome Powell, once again saved the day. During a recent U.S. Senate banking industry hearing, Jerome Powell suddenly announced that banks would not be subject to higher capital requirements. Remember, many politicians are calling for banks to hold more capital to avoid a repeat of the regional banking industry crisis of 2023. Clearly, banks lobbied hard to have these higher capital requirements removed. They have a good argument - if you, Bad Gurl Yellen, want us to buy shit government bonds, then we can only profit with infinite leverage. Banks around the world manage all types of governments; the United States is no exception.

The icing on the cake is a recent letter from the International Exchange Dealers Association (ISDA) advocating for the exemption of UST from the SLR I talked about earlier. Essentially, if banks are not required to make any down payment, they can only hold trillions of dollars of UST to finance the U.S. government deficit on a future basis. I expect the ISDA proposal will be accepted as the U.S. Treasury ramps up debt issuance.

Image source: Arthur Hayes

Image source: Arthur Hayes

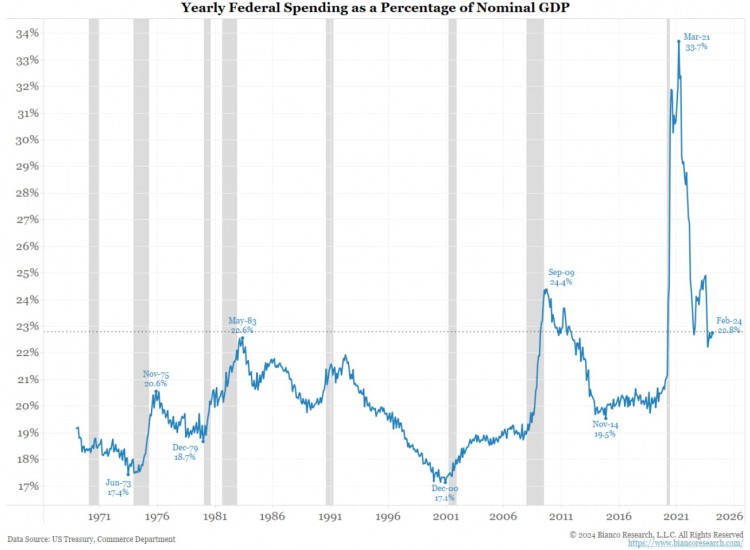

This excellent chart from Bianco Research clearly illustrates the extent of waste in the U.S. government, as evidenced by record-high deficits. The last two periods of higher deficit spending were driven by the 2008 global financial crisis and the baby-boomer-led coronavirus lockdowns. The U.S. economy is growing, but the government is spending like it's a depression.

All in all, the relaxation of capital requirements and the possible future exemption of USTs from SLR is a covert way of printing money. The Fed doesn't print money, instead the banking system creates credit money out of thin air and buys bonds, which then appear on their balance sheets. As always, our aim is to ensure that government bond yields do not rise above nominal GDP growth. As long as real interest rates remain negative, the prices of stokes, cryptocurrencies, gold, etc. will continue to rise in fiat currency terms.

壞女孩——珍妮特·路易斯·耶倫

My article "Bad Gurl" delves into how the U.S. Treasury Department, led by Bad Gurl Yellen, is increasing the issuance of short-term Treasury bills (T-bills) to deplete the trillions of dollars locked up in the Fed's reverse repo program (advice retail price). As expected, the decline in MSRP coincided with gains in stocks, bonds, and cryptocurrencies. But now that MSRP has dropped to $400 billion, markets are wondering what the next source of fiat liquidity will be to boost asset prices. Don't worry, Yellen hasn't finished yet, shouting "The loot is about to drop."

RRP balance (white) vs. Bitcoin (yellow)

Image source: Arthur Hayes

Image source: Arthur Hayes

The statutory funding flows I will discuss focus on U.S. tax payments, the Fed's quantitative tightening (QT) program, and the Treasury General Account (TGA). The timeline in question is from April 15 (the tax due date for the 2023 tax year) to May 1.

Let me help you understand what these three things mean by providing a quick guide on their positive or negative impact on liquidity.

Paying taxes removes liquidity from the system. This is because taxpayers must take cash out of the financial system, such as by selling securities, in order to pay their taxes. Analysts expect tax payments to be higher in the 2023 tax year due to large interest income received and solid stock market performance.

QT removes liquidity from the system. As of March 2022, the Fed is allowing approximately $95 billion worth of UST and MBS to mature without reinvesting the proceeds. This causes the Fed's balance sheet to decline, which, as we all know, reduces U.S. dollar liquidity. However, what concerns us is not the absolute level of the Fed's balance sheet, but the rate of its decline. Analysts such as Joe Kalish of Ned Davis Research expect the Fed to reduce the pace of QT by $30 billion per month at its May 1 meeting. A slower pace of QT would be positive for USD liquidity as the Fed's balance sheet decline slows.

When the TGA balance rises, it removes liquidity from the system, but when the TGA balance falls, it adds liquidity to the system. When tax payments are received by the Treasury, the TGA balance increases. I expect that with tax processing on April 15, the TGA balance will be well above its current level of about $750 billion. This is negative dollar liquidity. Don’t forget this is an election year. Yellen's job is to get her boss, President Joseph Robinette Biden Jr, re-elected. That means she must do everything she can to stimulate the stock market and make voters feel rich, and attribute this great result to the slow-moving “genius” of Biden’s economics. When the RRP balance finally drops to zero, Yellen will spend the TGA, likely releasing an additional $1 trillion of liquidity into the system, which will boost the market.

The period of instability for risk assets is from April 15 to May 1. At this point, the tax will remove liquidity from the system, QT will continue to run at its currently higher rate, and Yellen has not yet begun to reduce TGA. After May 1, the pace of QT slowed down and Yellen was busy cashing checks to drive up asset prices. If you are a trader looking for the right time to take a shameless short position, April is the time. After May 1, it's back to business as usual planning... asset inflation initiated by the financial shenanigans of the Fed and the US Treasury.

Bitcoin Halving

The Bitcoin block reward is expected to be halved on April 20. This is seen as a bullish catalyst for the cryptocurrency market. I agree that it will push prices higher in the medium term; however, the price action before and after is likely to be negative. The argument that halving is good for cryptocurrency prices is well established. When a majority of market participants agree on a certain outcome, the opposite often occurs. This is why I believe Bitcoin and cryptocurrency prices in general will plummet around the time of the halving.

Given that the halving occurs at a time when USD liquidity is tighter than usual, this will add fuel to the frantic sell-off in crypto assets. The timing of the halving further adds to my decision to abandon the trade before May.

So far I have made full profits on positions $MEW, $SOL and $NMT. Proceeds are deposited into Ethena's $USDe and staked to earn huge yields. Before Ethena, I held $USDT or $USDC and got nothing, while Tether and Circle got the full treasury yield.

Can the market overcome my bearish bias and continue higher? Fucking yes. I've always been passionate about cryptocurrencies, so I welcome mistakes.

Do I really want to take care of my most speculative shitcoin position when I'm two-stepping in Token2049 Dubai? Definitely not.

Therefore, I sold to clear my position.

There is no need to feel sad.

If the USD liquidity scenario I discussed above comes to fruition, I'll be more confident in imitating all kinds of shit. If I miss out o